Former Timesman Peter S. Goodman is out of the gates fast over at The Huffington Post.

He points out the hypocrisy of Republicans calling for investigations of Elizabeth Warren and her setting up of the Consumer Financial Protection Bureau. Supposedly she’s not being “transparent” enough. The gall! Compare that to, say, Dick Cheney’s doings, Goodman says:

Recently enough that you may still recall it, a secretive, paranoid man who had previously headed a major multinational energy company found himself vice president of the United States. This man deliberated privately with the heads of major oil companies as his administration set up a new energy policy that, perhaps coincidentally, wound up being strikingly generous to oil companies. The same man played a crucial role in leading the nation into a disastrous and costly war in a country that — again, perhaps coincidentally — held the world’s second-largest oil reserves.

And he lands a blow on the Obama administration while getting to the GOP:

Far be it from anyone to defend the Obama Treasury against charges that it lacks transparency. From its handling of its feckless homeowner-aid program, sold as a fix to the foreclosure crisis, to its administering of the Wall Street bailouts begun by its predecessors, this Treasury has been a maddening and combative model of misinformation, evasion and outright dishonesty. Again and again, it has sided with Wall Street over the public’s right to know, protecting Goldman Sachs and Bank of America in much the same way Dick Cheney lavished his nurturing ways on Halliburton and Exxon.

But this idea that Republicans in Congress are now pursuing the public interest in challenging Warren’s authority, trying to derail her devious plot to make the world safe for people with credit cards and bank accounts, is nothing short of hilarious. It is a brazen exercise in what regular people call balls, one that must be admired for its sheer, breathtaking nature.

Indeed.

— Thomas A. Cox, the Maine attorney who helped blow the foreclosure scandal wide open, writes an excellent post for New Deal 2.0 about how utterly stupid the banks can be in taking people’s houses away.

A woman couldn’t pay the $28,000 second note on her $48,000 house. She was still current on the first mortgage, on which she owed a bit more than the house was worth.

She was having trouble accepting the fact that it would really evict her, since she owed $50,000 on her first mortgage to a local bank, a loan on which she was current in her payments, which meant that KeyBank could recover nothing by foreclosing on its second mortgage. She told me again how, even though she had lost her job in the local paper mill, she had found other, but much lower, employment income and that she was able and willing to make reduced payments on the second mortgage. But KeyBank refused to accept reduced payments.

KeyBank, which owned the second mortgage, foreclosed on the woman anyway, despite the fact that it would lose far more money than if it had just walked away. Cox runs the numbers:

After spending over $4,000 on foreclosure costs and legal fees, it purchased my client’s interest in the property at its foreclosure sale (there were no other bidders for this worthless second interest) and it did evict this woman from her home at the beginning of October. She is now living in the basement of her daughter’s house. Since the interest in this home that it purchased was still subject to the outstanding first mortgage, it then paid $50,000 to the first mortgage holder so that it could own full title to the property as it made plans to re-sell it. Thus, at this point it had over $54,000 invested in gaining full title to this property. Last week, KeyBank listed this property for sale for $44,000. It will surely net no more than $40,000, if it can sell it at all. This will leave the bank with a real cash loss of over $14,000, a woman living in her daughter’s basement who was willing to pay at least some level on her second mortgage, her community with an empty and devalued property in its midst, and a very sour taste for all of us who try to help these people.

This, to put it kindly, is idiotic. You’d think Key Corp.’s shareholders might have something to say about that. Oh, who am I kidding?

Read Cox’s whole piece, which is one of the better op-eds I’ve read in a while. Here’s hoping we see more from him.

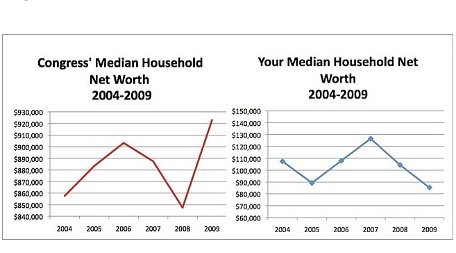

— The bottom 99 percent are doing poorly in the wake of this finance-led recession. The top 1 percent are doing just fine—and that includes many (most?) of our elected representatives.

Jesse’s Cafe Americain has the chart of the day on that, using Open Secrets numbers.

I almost don’t need to say this, but you think there might be a connection between that and the lack of urgency on the unemployment front?

Ryan Chittum is a former Wall Street Journal reporter, and deputy editor of The Audit, CJR’s business section. If you see notable business journalism, give him a heads-up at rc2538@columbia.edu. Follow him on Twitter at @ryanchittum.