Fortune again.

This time it’s Geoff Colvin, passing along the Chamber of Commerce line that “Uncertain of future regulation, businesses are paralyzed.” He’d have you think that this is much of the reason the economy is struggling.

Here’s the lede:

Dick Kelly wishes he knew what his industry should do. “If we had a national policy and knew what the rules were, we could take action,” says Kelly, CEO of Xcel Energy and chairman of the Edison Electric Institute, the association of shareholder-owned electric utilities. But Kelly’s industry knows only that momentous changes in the federal laws governing it are probably on the way; what those changes might be, and when they might happen, managers have no idea. So they “are holding up decisions,” Kelly says, on multibillion-dollar investments to convert old coal-fired power plants to natural gas. “Is there going to be a price on carbon?” he asks. “Will there be a timeline? Will we have to use a certain percentage of renewables?” No one knows, so nothing is happening.

Multiply the utilities’ experience across the economy, and we begin to see an important reason why growth is getting slower rather than faster as the recovery creeps along. When people aren’t sure what’s going to happen, they freeze.

Left out here, naturally, is that lobbying funded by businesspeople like Kelly is one of the major reasons we don’t have an energy bill. But really is it so hard to figure out what you ought to do? Carbon-intensive energy production is going to be more expensive in the future. Produce much less of it.

Colvin just misleads on that McDonald’s health-care nonstory in a bid to make his case:

McDonald’s recently said it might drop medical coverage for 30,000 employees because of a rule buried in the new law.

Again, no it didn’t. It said it might switch health plans.

Then there’s this:

Life is inherently uncertain, of course, but this is different. As I travel around the country, businesspeople tell me they’ve rarely felt so unsure of what the laws and rules governing their business will be. Like Kelly, they sense major changes ahead — but what? So instead of investing and hiring as usual in a recovery, U.S. companies are sitting on more cash than ever. We shouldn’t be surprised. It has always been true that the more activist the administration in Washington, the more uncertainty it spawns.

Get that? The reason businesses are sitting on cash isn’t that the economy is still severely overleveraged with no obvious paths for growth, it’s that some rules are going to be changing here and there (indeed most of the reforms, besides energy, have already been passed, and they’re hardly punitive to business interests).

I have no doubt that businesspeople really are saying this stuff to Colvin. They may actually think it. Having interviewed and broken bread with way too many of them myself, I can testify to how quickly they latch on to the conventional wisdom bouncing around certain circles. I don’t know how many times I had to stifle a chuckle, for instance, when talking to some executive who brought up Tom Friedman’s The World Is Flat nonsense as gospel back in the middle of the last decade.

I also learned that businesspeople are really the best at making excuses and blaming other people or phenomena for their failures. They’re also used to getting their way and don’t like it when somebody tells them they can’t do something anymore—like, I don’t know, gouge customers with overdraft fees, or burn up the atmosphere with coal-fired power plants.

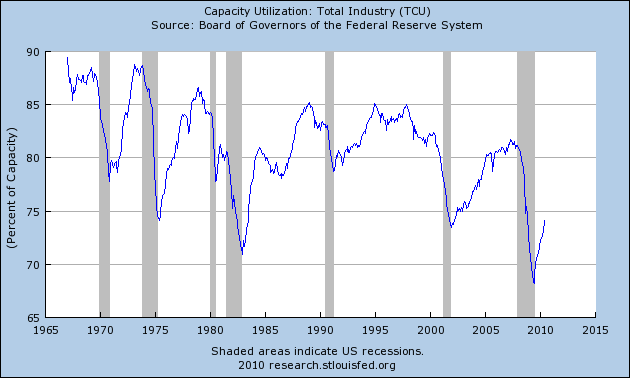

Certainly regulation and the prospect thereof has a big impact on business decisions, especially when these guys are used to dictating what happens in Washington and installing their colleagues as regulators (which raises the minor point that there was some business uncertainty during the Bush administration, too: Just how far can these guys bend over backward for us?). But it’s hard to imagine that this is the major reason the animal spirits are so wounded these days. Here are some other major things not mentioned by Colvin that are bigger problems: deflation, an indebted and weak consumer, massively underutilized capacity.

{kind=link}

I’ll leave the rest to Invictus over at Barry Ritholtz’s place, who smacked this line down when Fareed Zakaria wrote something similar three months ago. One of the many things Invictus pointed out was an annual survey of the “single biggest problem” facing small businesses—you know, the ones who create most of the jobs:

You’ll note that Poor Sales were at 30 one year ago, and remain there now. “Govt Regulations and Red Tape” were at 13 one year ago and remain there now. Taxes were at 19 one year ago and have ticked up to 22. So there have been no changes in the rank of these three problems from the year ago snapshot; they rank today as they ranked then…

I’ll readily stipulate that large businesses and small businesses have both their similarities and their differences. But I have a hard time believing that those differences are so great that larger companies’ biggest concerns are taxes and regulations while small companies are worried about poor sales.

Indeed, and Colvin might want to explore what I suspect is an even bigger damper on the economy: Mistrust of the Big Business folks (“pragmatic managers who want to make an honest buck,” Colvin trusts) he’s made a career of pow-wowing with. Talk about uncertainty. Is my bank going to screw me over? Can I trust that mortgage servicer? Why should I invest capital in a rigged stock market?

Thing is, you’d have to get out there and talk to customers rather than CEOs to hear that stuff.

Ryan Chittum is a former Wall Street Journal reporter, and deputy editor of The Audit, CJR’s business section. If you see notable business journalism, give him a heads-up at rc2538@columbia.edu. Follow him on Twitter at @ryanchittum.