Martin Wolf’s weekly column alone is worth paying for a Financial Times subscription. Or if you visit FT.com just for that you can get them all for free (the site gives you ten stories a month gratis). His effort today is a good example why you should bookmark him.

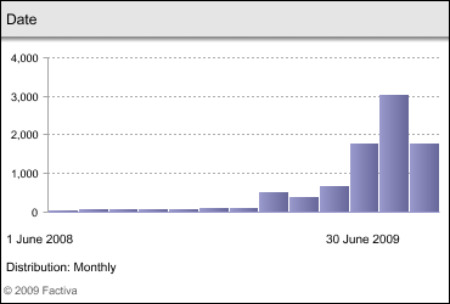

First, I’ll note that I’ve been very skeptical about all the “green shoots” jibber-jabber that’s filled news pages in the past three months, so I’m predisposed to like this Wolf column. See this Factiva chart of how many times it’s appeared in the press over the last year:

It’s dangerous for the media to buy into false optimism. The public will not be kind if we head south again. Wolf explains why we’re far from out of the woods, pointing out that this downturn is in some ways worse than the Great Depression. The only thing keeping the bottom from utterly falling out is the massive government spending and backstopping that’s gone on in the last nine months.

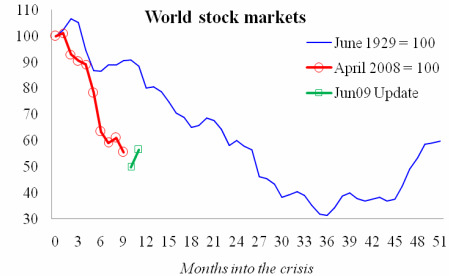

Green shoots are bursting out. Or so we are told. But before concluding that the recession will soon be over, we must ask what history tells us. It is one of the guides we have to our present predicament. Fortunately, we do have the data. Unfortunately, the story they tell is an unhappy one.

Unhappy indeed: Stocks down worse than the Great Depression. Global trade down far more. Industrial output down as much as back then. Top-hat sales plummeting. Monocle industry in peril. Moustache wax inventories building. Etc.

Check out the charts from economists Barry Eichengreen and Kevin H. O’Rourke, which Wolf links to, that plot the state of the economy and markets against the same timeframe as the Great Depression. Don’t misplace your happy pills.

As Wolf points out, we’re in something like the eye of the storm right now. So much government money has been pumped into the system—something he applauds—that it pretty much had to stabilize.

During the Great Depression, the weighted average discount rate of the seven leading economies never fell below 3 per cent. Today it is close to zero…

…during the Great Depression, money supply collapsed. But this time it has continued to rise.

And Keynesian government spending on stimulus and other programs has been much higher now than back then.

But all those trillions of dollars come with their own day of reckoning. The problem is, we don’t know when that is or what form it will take, Wolf says: Take away the punch bowl too soon and the economy tumbles. Take it away too late and you get inflation with no growth—that nasty word stagflation—plus a public debt problem that could be crippling.

Either way, the economy is in for a long hard slog, and that’s something the press, with its institutionally short attention span, needs to keep in mind:

Robust private sector demand will return only once the balance sheets of over-indebted households, overborrowed businesses and undercapitalised financial sectors are repaired or when countries with high savings rates consume or invest more. None of this is likely to be quick. Indeed, it is far more likely to take years, given the extraordinary debt accumulations of the past decade.

Wolf does a superb job of explaining all this dismal science stuff for the lay reader. It’s about as sharp as column-writing gets. For instance, his kicker—another slapdown of the green-shoots Pollyannas:

Ryan Chittum is a former Wall Street Journal reporter, and deputy editor of The Audit, CJR’s business section. If you see notable business journalism, give him a heads-up at rc2538@columbia.edu. Follow him on Twitter at @ryanchittum.Last year the world economy tipped over into a slump. The policy response has been massive. But those sure we are at the beginning of a robust private sector-led recovery are almost certainly deluded. The race to full recovery is likely to be long, hard and uncertain.