The Wall Street Journal credulously reports on a new paper by Columbia B-school professor Charles Calomiris on why we have lots of banking crises while our friendly neighbors to the north don’t.

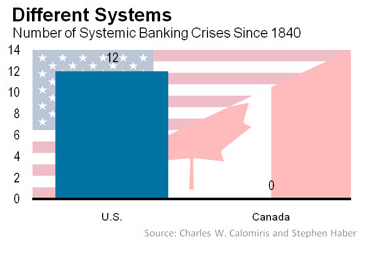

Calomiris says that we’ve had 16 systemic banking crises since 1790 while Canada has had none. Like, zero, according to the WSJ’s weirdly bad graphic:

I’m no expert on Canadian banking history, but is it true that they’ve never had a banking crisis? Calomiris himself writes that “Canadian banks, throughout their history, avoided systemic banking crises – with the exception of two short-lived suspensions of convertibility in 1837 and 1839 in response to crises originating in the United States.”

But there was also a severe financial crisis in 1907 where the government had to step into bail out banks, and ninety percent of Canadian banks were insolvent in the 1930s but held afloat by regulatory forbearance, according to Lawrence Kryzanowski and Gordon S. Roberts.

As they write:

…the superior performance of Canadian banks in avoiding explicit failure should be attributed to the Canadian government’s policy of encouraging the early merger of troubled and healthier banks, standing ready to lend to banks, and providing an implicit one hundred percent guarantee of bank deposits by effectively guaranteeing all deposits at par.

Kryzanowski and Roberts essentially argue, Canada’s banks were too big to fail and were given implicit government guarantees. By that logic, if there was no Canadian banking crisis in the 1930s, then there was no American banking crisis in 2008 (Lehman being the exception that proved the rule)—something few would argue.

Canada also quietly bailed out its banks in 2008. Was that not a crisis? In other words, Canada did indeed have banking crises, but was able to prevent them from becoming banking panics in the last century has been in no small part because of its willingness to socialize risk and losses and oversee acquisitions of weak banks.

And yet Calomiris writes that “the stability of Canada’s banks was accomplished with little government intervention, either in the form of prudential regulation or assistance to distressed banks.” Canada, the AEI’s laissez-faire paradise. Really? That Canada has barely regulated its banks is not true, even according to its own conservative prime minister.

But that’s actually the least of my concerns here. The red flags come right away in the WSJ’s piece as it reports Calomiris’s explanation of how Canada supposedly got so crisis-free:

British policymakers steered toward a government structure that would limit the power of the French-majority while also giving Canada more and more self-government. The eventual result was a highly-centralized federal government which controlled economic policy making and had built-in buffers for banker interests against populist forces, the paper argues.

So banker interests are associated with stability and “populist” interests are associated with financial crises? War is peace and all that.

Populist democracies like the U.S., on the other hand, tend to create dysfunctional banking systems because a majority of citizens gain control over banking regulation that steers credit to themselves and to their friends at the expense of the citizens that are excluded from the banking system, he said.

The idea that “citizens” have “control” over the U.S. financial system doesn’t even pass the laugh test. The Fed is about as unpopulist an institution as you could design and traditionally leans far more toward preserving the value of capital than it does toward boosting unemployment. And the idea of the U.S. as a populist democracy is hard to square with the reality of the US Senate, specifically designed as a break on popular passions, where the median net worth of a senator is $2.5 million. The average net worth is $14 million, and the Democrats–supposedly our country’s labor party–are richer than the Republicans. In the “populist” House, the median net worth of a representative is $856,000, 13 times the median American household. The Fed leans more toward preserving the value of capital than it does toward boosting employment.

It’s not as if the WSJ was misreading Calomiris. One of the main sections of his paper is headlined, “The Crippling Influence of Populism in U.S. Banking History.”

Calomiris writes in his paper that from the time of Andrew Jackson “until roughly 1980–the coalition of small bankers and agrarian populists would dominate the politics of bank chartering and bank regulation in the United States,” which is a rather selective reading of U.S. financial history.

If you’ve been paying attention to the last five years of conservative rationalization of the financial crisis, you might be able to guess where this is going. What Barry Ritholtz has called the Big Lie of the Crisis—pushed primarily by Calomiris’s colleagues at the American Enterprise Institute—says that it was the government, not a runaway financial sector, that created the subprime mortgage bubble and resulting financial crisis. You know, Fannie, Freddie, and the Community Reinvestment Act, rather than Citigroup, Countrywide, and the Commodity Futures Modernization Act. This has been debunked so many times (including by the WSJ itself) it’s almost malpractice for the Journal not to note it, much less not to disclose Calomiris’s AEI affiliation:

Mr. Calomiris argues that in the U.S., a coalition that emerged in the 1990s of government, big banks and activist consumer groups came helped fuel the housing crisis. Regulatory changes opened the door to a wave of mergers and acquisitions that created today’s megabanks. But banks still had to get approval – usually from the Federal Reserve—to complete those mergers and outside groups were able to weigh in on the wisdom of the deal as part of the Fed’s decision-making process.

Community groups, with the Clinton administration’s encouragement, used the Fed’s approval process to extract binding concessions from banks to loosen underwriting standards for poor, urban communities—concessions to which the Fed agreed, Mr. Calomiris argues. The banks had to apply the looser standards to everyone. That helped fuel an explosion in poorly underwritten mortgages that contributed to the depth and severity of the housing crisis, he contends.

The WSJ can’t be bothered to pass along the context that Calomiris’s views are beyond controversial; they’ve been roundly debunked. As though it was ACORN and the NAACP, rather than Wall Street, that were the real muscle behind Riegle-Neal, the CMFA and Gramm-Leach-Bliley, the advent of credit-default swaps and synthetic mortgage-backed securities, preemption, regulatory capture, predatory lending, and too big to fail banks.

Take the Community Reinvestment Act, to which Calomiris devotes most of six pages of his paper, arguing that it was essential in spurring the kind of risky lending that caused the subprime crisis. But this is transparently bogus, as we and many others, including the Federal Reserve and conservative Chicago economist Randall Kroszner, have pointed out many, many times. CRA-subject lenders were responsible for just 6 percent of subprime mortgages in 2005 and 2006, suggesting “it is very unlikely the CRA could have played a substantial role in the subprime crisis… Rather, it is likely that higher-priced lending was primarily motivated by its apparent profitability.” That doesn’t mean 6 percent of all subprime mortgages were because of the CRA, it just means that 6 percent is the maximum possible. The actual CRA-triggered amount would be much, much lower.

The Calomiris thesis is no less than an audacious attempt to apply the AEI’s crisis thesis to nearly the whole of American financial history and to argue that it was anti-democratic policies that have stabilized Canada’s bans and democratic ones that have destabilized American ones.

A thesis as controversial as that—particularly one with holes so easily poked in it—deserved far greater scrutiny by the Journal.

(Updated to tweak the headline)

Ryan Chittum is a former Wall Street Journal reporter, and deputy editor of The Audit, CJR’s business section. If you see notable business journalism, give him a heads-up at rc2538@columbia.edu. Follow him on Twitter at @ryanchittum.