Sign up for the daily CJR newsletter.

Cheyenne Hopkins of American Banker, who first published the terms of the proposed mortgage servicer settlement in March, has now got her hands on a ridiculous paper from Charlie Calomiris, Eric Higgins, and Joseph Mason, which says that the settlement is a bad one which could cost the economy $10 billion a year.

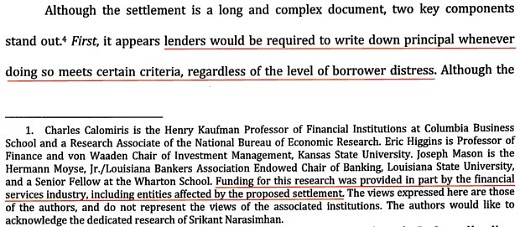

You only need to look at the bottom of the first page of the paper to see where this thing is going.

First of all, there’s nothing in the proposed settlement saying that principal write-downs should be conducted “regardless of borrower distress.” To the contrary, the talk of principal reductions explicitly applies only to delinquent mortgages. Which actually the authors know full well, since on page 10 they say that “the settlement’s approach to loan modifications would encourage strategic default.” They can’t really have it both ways.

As for the fact that the paper was bought and paid for by the very banks opposing the settlement, Mason tells Hopkins that “we never allow any funder to dictate our conclusions.” But of course he doesn’t need to, since the authors know full well what they’re expected to produce. It’s basically a variation on that notorious Greenspan op-ed: attempts to regulate the financial services industry have failed in the past, therefore there’s no point in even trying any more.

Some of what the authors write about loan servicers defies belief:

NPV calculations are already used by servicers, exercising their fiduciary duty to maximize the value of payouts to investors, in determining whether a borrower qualifies for a loan modification…

That servicers have not modified more loans indicates that, under their NPV analyses, additional modifications would not result in higher payouts for investors, despite the benefits of avoiding a protracted and expensive foreclosure process…

Servicers already use NPV analyses as a matter of course. If a servicer finds a modification to be NPV-positive, then it will likely modify the loan without any regulatory oversight.

Even bankers aren’t making these arguments with a straight face any more. But, as HL Mencken famously said, there is no idea so stupid that you can’t find a professor who will believe it — and the banking industry, here, seems to have found just those professors.

In fact, this isn’t stupidity: Calomiris et al aren’t stupid. But it’s intellectual dishonesty: they know full well about the various lawsuits and other attempts that mortgage-bond investors are making to get servicers to change their ways, and they also know full well that banks’ servicing departments are badly-run and fundamentally broken. But somehow, after taking a long bath in bankers’ dollars, they’ve managed to persuade themselves that those banks always exercise their fiduciary duty to investors and never foreclose when doing so makes little financial sense. (And, for that matter, they’ve also persuaded themselves that taking large amounts of money to write papers for the financial services industry has no effect on what they end up writing.)

As for the authors’ attempts to quantify the costs of the settlement, they use numbers in the CFPB report uncovered by Shahien Nasiripour which says that “effective special servicing of delinquent loans would have cost 75 bps/yr more than the actual costs incurred” — except the way they put it is very different:

The CFPB recently estimated that five servicers avoided $24 billion in costs between 2007 and 2010, yielding a 75 basis-point reduction in interest rates.

Er no, the CFPB nowhere says or even hints that there was any kind of reduction in interest rates as a result of the banks’ broken servicing operations. (And it wasn’t five servicers, it was nine.)

I’m also particularly fond of the way that the authors calculate the increase in foreclosure inventory brought on by an increase in strategic defaults. “For simplicity,” they say in footnote 48, “we assume all strategic defaults result in foreclosure.”

What?

The entire reason why strategic defaults would go up, according to the paper, is that borrowers will know that if they default, they’ll get a loan modification. And yet somehow by the time we reach footnote 48, all those borrowers are mistaken, and in fact they won’t get a loan mod: they’ll be foreclosed upon instead.

It’s unclear whether this paper was ever intended for public consumption, or whether it’s just something for banks to quietly pass on to their lobbyists, who in turn will show it to lawmakers. But it’s certainly harder to take Calomiris seriously in his attempts to revisit Dodd-Frank when he’s happy churning out hack-work like this which shows him to be completely captured by Wall Street.

Has America ever needed a media defender more than now? Help us by joining CJR today.