Steven Pearlstein goes into his columnists’ bag of tricks to show how crazy Governor Scott Walker’s agenda would be if a Democrat tried to pull it:

One old trick is to suggest a thought experiment that asks readers to consider the mirror image of what is going on. In this case, you’d be asked what the reaction would be from Republicans and business interests if a newly elected Democratic governor and legislature proposed to deal with a budget deficit by first raising unemployment benefits and then pushing through a big corporate tax increase for all but the Democratic-leaning tech sector. For good measure, the package would also contain a ban on corporations making political donations without getting the permission of each shareholder, lest they use their power to repeal the tax increase and push the budget out of balance.

This is analogous, of course, to what Gov. Scott Walker has proposed for dealing with Wisconsin’s budget gap: the tax breaks for businesses, the benefit cuts for all state employees except Republican-leaning police and firefighters, the automatic decertification of all public-sector unions and the stripping of their right to bargain anything but wages. Looking at Walker’s reflection in the political fun-house mirror makes it abundantly clear that the governor has a more ambitious agenda than merely closing a modest budget gap.

It takes some incredible chutzpah to take a crisis caused by Wall Street capitalists and right-wing ideologies and use it as an excuse to squash what remains of the American labor movement.

— Speaking of Wisconsin’s governor, the Society of Professional Journalists is out with a statement blasting a journalist who snookered Walker into thinking he was a right-wing billionaire.

The Society of Professional Journalists, through its Ethics Committee, strongly condemns the actions of an alternative online outlet this week when an editor lied and posed as a financial backer in a recorded phone call with Wisconsin Governor Scott Walker.

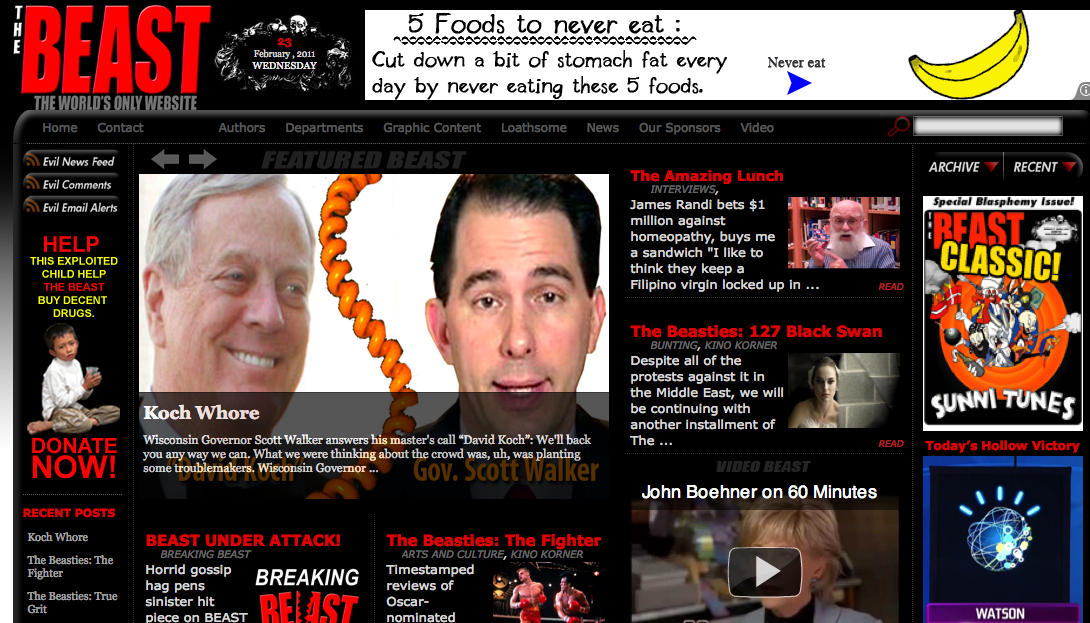

Thing is, I’m pretty sure said alternative online outlet, aka the Buffalo Beast, doesn’t care what SPJ thinks about how to do journalism. Here’s a screen shot of its home page:

Yes, the headline next to the main “Koch Whore” story says “Help this exploited child help The Beast buy decent drugs.” The Buffalo News it ain’t.

Its blogger, noting that Democratic leaders in the state hadn’t been able to get hold of Walker via phone, told the governor’s receptionist that he was conservative billionaire David Koch and was promptly put through to the governor himself.

That bit of gonzo is as revealing as a hundred straight-news stories, no?

— And to round out our all Upper Midwest edition of Audit Notes, Brian J. O’Connor of The Detroit News does a good job keeping an eye on how banks are going after borrowers even after foreclosures and short sales. I don’t think many people understand this can and is happening and this kind of story is what the press needs to be doing:

Now, because of dropping property values, mortgage lenders are engineering foreclosures so they can pursue a borrower for the unpaid balance of a home loan for years to come. With added fees and interest, this phantom debt — called a “mortgage deficiency” — could swell to become more than the homeowner paid for the property.

Here’s how it works:

But now that many homes in the region are worth far less than their mortgages, lenders aren’t bidding what’s owed. They enter bids for the current value of the home or, sometimes, even less. Under state law, the lenders can then pursue the homeowner for the shortfall between what was owed and what the lender got when the home was sold, plus legal fees and interest.

Lenders have up to six years to sue for the bad debt and, once they obtain a judgment, can pursue the borrower for 10 years. If they still haven’t collected, they can renew the judgment for another decade, repeating the process indefinitely.

During that time, interest can build on the debt at the default rate stated in the original mortgage. That’s usually four or five percentage points above the original mortgage rate, so a deficiency on even a low 6-percent loan would be charged 10 percent or 11 percent interest, doubling the cost of the debt in as little as six and a half years.

O’Connor reports that one of the biggest problems is bottom-feeding collections agencies buying bad debts for pennies on the dollar.

Ryan Chittum is a former Wall Street Journal reporter, and deputy editor of The Audit, CJR’s business section. If you see notable business journalism, give him a heads-up at rc2538@columbia.edu. Follow him on Twitter at @ryanchittum.