Sign up for the daily CJR newsletter.

Martin Peers had a smart Heard on the Street in yesterday’s Wall Street Journal on the critical question of how much of the recent plunge in media companies’ fortunes has been a cyclical decline versus a secular one.

It’s obviously some of both, but the mix will decide what the next five years look like for magazines and newspapers, the critical providers of original reporting in the country. Alas, I’ve crunched some numbers on the industry and they’re beyond ugly.

First, some definitions. A cyclical decline is one due to the inevitable ups and downs of the broad economy. Most businesses get hurt in the recession part of a cycle but do well in the expansionary part and their fortunes more or less move up or down with the economy at large.

But structural changes in the economy or a specific industry can result in secular changes for a business. Think for instance, the classified-ads business of newspapers, which has been walloped by eBay and craigslist (with a final indignity provided by the cyclical collapse of the housing bubble). Most of those revenues aren’t coming back. That’s a secular decline.

Overall daily newspaper-industry ad revenue just flat-out crashed last year, plunging 16.7 percent to $37.8 billion from $45.4 billion in 2007, which itself was a bad year with ads down 7.9 percent from $49.3 billion in 2006.

It gets worse. So far 2009 has been more dismal than 2008. Alan Mutter predicted in January that newspaper revenue would tumble 17.3 percent this year to $31.6 billion, or just below 1993 levels. If anything, his numbers may be optimistic. Several major newspaper companies have reported declines of about 30 percent so far this year.

But even that $31.6 billion understates just how awful the numbers are. Remember $31.6 billion in 1993 bought a whole heckuva lot more than $31.6 billion does today—49 percent more to be exact.

So I went back through the Newspaper Association of America’s data on newspaper-industry revenue, which goes back to 1950, to see what year we’re actually even with now. It’s ugly: You have to go back to 1965 to find a year with revenue lower in 2009 dollars than what this year is projected to be. That year, the industry took in $4.42 billion, which works out to $30.22 billion in current dollars. The industry can only hope this year hits 1966 levels, which work out to $32.4 billion in real dollars. (A caveat: there are fewer papers now than there were in 1965 and production is more efficient.)

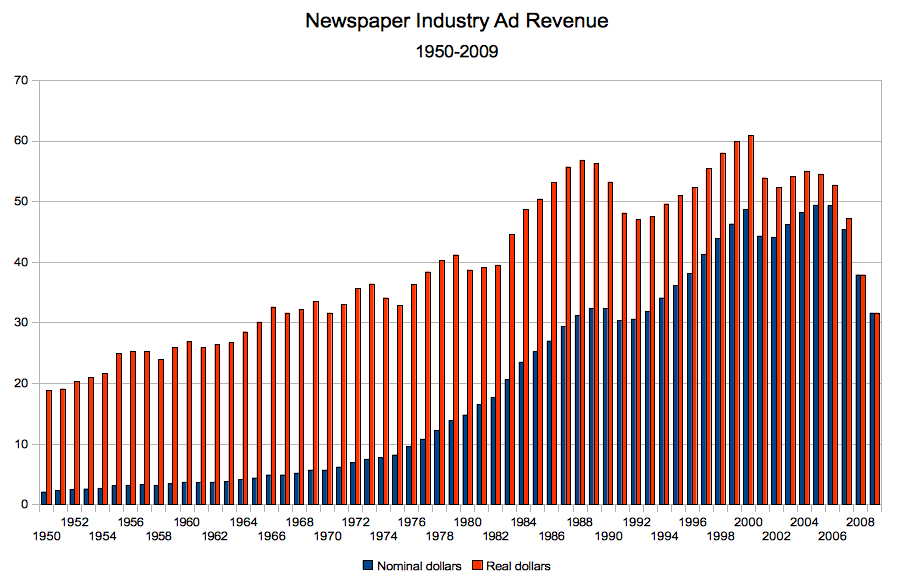

Here’s a chart I cobbled together that illustrates the disparity between nominal and real (inflation-adjusted) numbers. Note: the 2009 number is Mutter’s $31.6 billion estimate. Click the chart for a bigger image:

What stands out immediately to me looking at real dollars (which are all that really matter), is that the peak of the last recovery, in 2004, with $55 billion, never got close to the peak of the previous recovery, 2000—when real ad revenues hit $60.9 billion. To make matters worse, the 2002-2004 recovery never reached the peak of two recoveries ago, in 1988, when real ad dollars hit $56.8 billion. Recall, this year ads are projected at just $31.6 billion—if they’re lucky—a 44 percent decline from twenty-one years ago.

That folks, is secular decline, and the vast majority of those dollars are not coming back.

You’ll see, as well, if you trace a line across the chart, that the last time ad revenues were lower than the estimated 2009 total was forty-four years ago (they tied it in the recession of 1970), when they were $30.1 billion.

This is the state of the business today. One recent study by Borrell Associates (see chart below) predicts that newspaper ads have hit bottom and will edge up in the next few years. That would be great, but nobody can predict a bottom in any market, especially one with as many unknowns as the newspaper industry—and in an economy as uncertain as this one.

Newspapers need a rip-roaring recovery to recover a small portion of the ground they’ve lost, and I doubt they’re going to get it. Barring that, they have to staunch circulation declines to try to manage the longer-term decline of the print business, which, after all still has 48.6 million* readers paying for the newspaper every day. Certainly, the devastated economy has been a significant factor in pushing down newspaper ads far below what the secular changes would have alone, but it’s clear the secular changes have been dominant.

As for the Journal’s Peers, his larger point is that the collapse has been so shocking it has forced media companies to own up to the fact that ad-only strategies aren’t going to cut it for many of them:

For investors, the positive development of the recession is how much it has changed attitudes about the Internet’s potential as a business model. After several years of acting like lemmings, offering some of their best content free online, both TV and print media executives are rethinking. It is now clear that Google’s spectacular success at building a highly lucrative business from its heavy Internet traffic was something of a one-off. Amassing a big audience online doesn’t yet guarantee enough ad revenues to sustain a big business.

That’s right. The industry got just $3.1 billion from online ads last year, a number that is on pace to decline significantly in 2009. Even that 2008 number was only about 5 percent of the industry’s peak ad revenues in 2000. Again, I’ll note that circulation revenues are the only part of the pie growing right now.

Tough business, no?

ADDING: If you want to look at the precise numbers I used and calculated, here’s my Excel spreadsheet (converted from OpenOffice, so hopefully it will work on Excel).

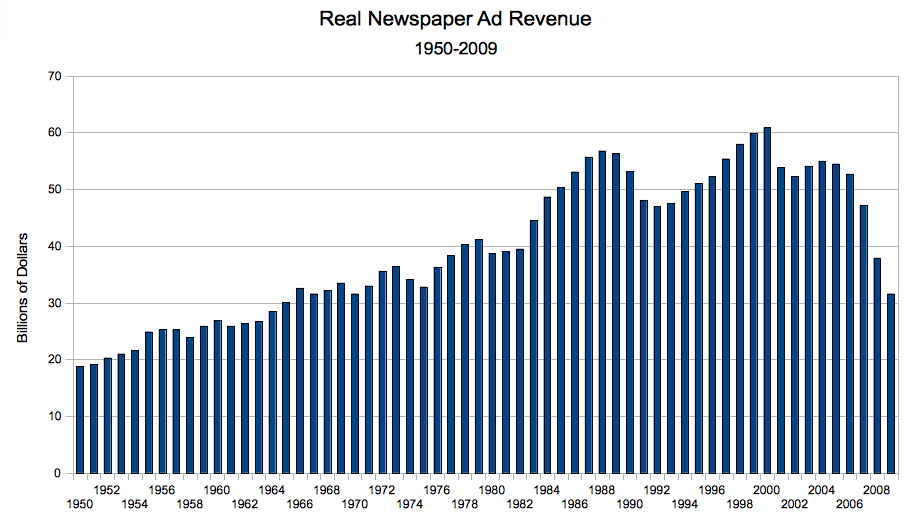

And here’s a chart with only the real ad revenue numbers (click to enlarge):

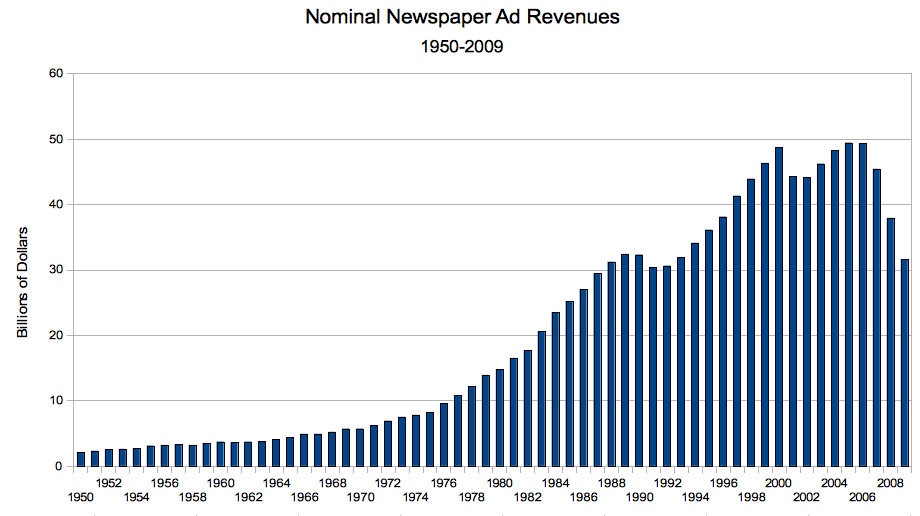

And one with just the nominal numbers:

* Corrected from 42.8 million to include evening-paper circulation

Has America ever needed a media defender more than now? Help us by joining CJR today.

{kind=link}

{kind=link}

{kind=link}