Sign up for the daily CJR newsletter.

Bloomberg’s Jonathan Weil wrote a swell column last week on the SEC’s latest Citigroup wrist-slap. Weil noted that one of the terms of the settlement was that Citi not violate the law again and reported that it was the fifth time in eight years that the same Citi subsidiary had settled with the SEC for violating the same law, each time promising not to do it again.

Which is a great catch.

Today The New York Times takes it on, broadens it, and gets a very good page one story out of it. Here’s what Edward Wyatt found:

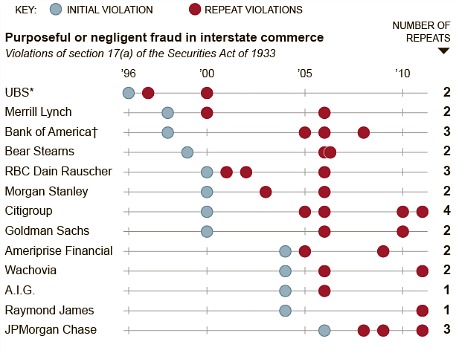

A Times analysis of enforcement actions during the past 15 years found at least 51 cases in which the S.E.C. concluded that Wall Street firms had broken anti-fraud laws they had agreed never to breach. The 51 cases spanned 19 different firms.

First, why make somebody promise not to break the law? “Okay, copper. I promise I’ll never rob another bank again if you just let me go this time.” Lawbreaking is illegal. I suppose the only possible reason is so you can come down harder on subsequent violations—like a probation.

The problem is, there’s no “or else” here. The Times notes that Judge Jed Rakoff, who’s been highly skeptical of the SEC’s weak approach, asked it if it’s filed contempt charges against any repeat violators. The answer:

The S.E.C. said in a court filing Monday that it had not brought any contempt charges against large financial firms in the last 10 years.

So what’s the point? The Times asks Robert Khuzami, the former Deutsche Bank top laywer (who dealt with at least some CDO stuff) turned SEC enforcement chief (emphasis mine):

Robert Khuzami, the S.E.C.’s enforcement director, said never-do-it again promises were a deterrent especially when there were repeated problems. In their private discussions, commissioners weigh a firm’s history with the S.E.C. before they settle on the amount of fines and penalties. “It’s a thumb on the scale,” Mr. Khuzami said. “No one here is disregarding the fact that there were prior violations or prior misconduct,” he said.

A promise is only a deterrent if you know violating it will incur increasingly unpleasant consequences, as any child could tell you.

As far as disregarding prior violations, here’s Weil on Citi:

The commission already had two cease-and-desist orders in place against the same Citigroup unit, barring future violations of the same section of the securities laws that the company now stands accused of breaking again. One of those orders came in a 2005 settlement, the other in a 2006 case. The SEC’s complaint last month didn’t mention either order, as if the entire agency suffered from amnesia.

Perhaps from now on the SEC should list in its complaints every violated promise by those with whom it’s settling.

Because there are a lot of repeat offenders, and the Times is smart to put them in a graphic.

Click through to see the whole thing.

Has America ever needed a media defender more than now? Help us by joining CJR today.