The price of housing, whether buying or renting, is rising, or so say many recent news reports.

Some skepticism is in order–and was, in some cases, provided (though it was the rising prices that largely led). Broader reporting on housing economics would help.

July housing prices went up at their fastest rate in seven years, as The Washington Post reported on September 24 (though the piece also noted that “economists say there are signs the housing market is beginning to cool.”) Prices may be “on track” to recovery, as The New York Times reported the same day (the Times also indicated “some analysts are worried [the housing market] may slow down in the months ahead.”) Housing prices may be slowing, is how USA Today had it.

No news report about housing prices is complete without some discussion of incomes. In the long run, housing prices must reflect the incomes people have to finance their residences–a basic economic fact neglected in these stories. And of the above pieces, only the USA Today report got at that (albeit very briefly):

Price gains need to slow even more to be sustainable, given flat incomes, says Stan Humphries, Zillow chief economist.

Elsewhere, Catherine Rampell’s Oct. 6th piece in The New York Times Magazine included some important insights–too often missing in routine coverage of housing prices–especially that “half of all homes that went into foreclosure between 2007 and 2012 were actually in the lowest price tier when they were purchased, and most were located in middle- and lower-income areas.”

Rampell’s line refers indirectly to how the worst mortgages during the era of inadequate-to-no-underwriting were sold to people who were unlikely to be able to pay the money back, especially when interest rate resets and additions to principle made the cost more than the borrowers could bear.

And, Rampell noted, “the boom-bust-flip phenomenon is just one of the most obvious ways that research suggests the financial crisis has benefited the upper class while brutalizing the middle class.”

But then Rampell writes, “Rents have risen at twice the pace of the overall cost-of-living index” and quotes an expert as saying landlords can raise rents “with impunity.”

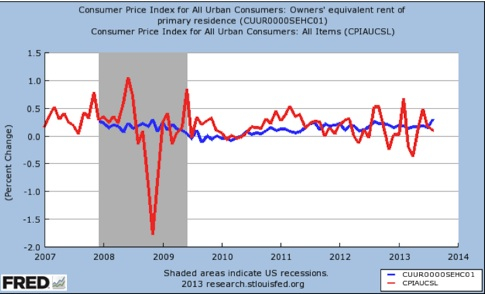

Below is the graphic I created at the St. Louis Federal Reserve website–graphics can easily be created using economic data at the site–which shows that the official data does not support what Rampell wrote. The red line is the monthly consumer price index, the most widely used inflation rate measure. The blue line is the monthly imputed rental value of owner-occupied housing, excluding the cost of utilities, a proxy for rents.

As the graph below shows, rents rose–and fell–but they did not grow at twice the rate of inflation. For short periods rents, and housing prices, can grow, or shrink, at very different rates than the overall economy, but in the long-run housing prices have to relate to real incomes.

A better piece than Rampell’s, because it looked at the issue from the perspective of would-be homeowners, ran appeared the same day by Pete Carey, the Pulitzer Prize-winning San Jose Mercury reporter (and my desk mate 45 years ago).

Carey looked at how many first-time buyers cannot afford a house in the San Francisco Bay Area, with data for four counties, and noted how high housing prices force people into the rental market, which, in turn, puts upward pressure on rents. He ended with this telling quote from the chief economist for the real estate website Trulia: “Rents are rising faster than incomes, and home prices are rising much faster than incomes.”

Again, housing prices cannot over the long run rise faster than incomes. And to the extent that they do, it depresses other spending, which means a weaker economy overall.

Every income group made significantly less in 2012 than in 2007, and all but the top one percent of the top one percent made less in 2012 than in 1999, analysis of tax return data by Professors Emmanuel Saez and Thomas Piketty shows.

The median income of the bottom 90 percent of Americans in 2012 was down $4,900 or almost 14 percent compared to 2007. Those on the 90th to 95th rungs of the income ladder were down 6.2 percent, data you can calculate at Table A6 of the Saez and Piketty report for 2012.

Since 2009, they show, 94.8 percent of all income growth has gone to the top one percent. What is even more revealing is how much of that went to the one percent of the one percent–31.7 percent.

In a nation with about 314 million people, fewer than 16,000 households enjoyed nearly a third of all the reported income gains since 2009. And the bottom 90 percent? The vast majority saw their incomes slip downward from $31,553 in 2009 to $30,997 in 2012, a decline of nearly two percent.

So what factors could propel housing prices, and rents, higher if incomes are down?

One is local conditions. There is no national housing market, only local ones. And prices vary enormously. I once looked at the cost of replacing my home in Western New York with one in Chevy Chase, Maryland, just outside the nation’s capital. Fully comparable homes were priced at about ten times the value of mine. That is one aspect of what the real estate industry says are its only three rules for immovable property: location, location, and location.

Another answer comes from Kate Berry of American Banker, who explained in April:

banks are walking away from thousands of vacant properties after starting and then refusing to complete the foreclosure process because they do not want to pay for maintaining the homes.

The result: hundreds of thousands of homes are being withheld from the market, raising questions about whether the recent run-up in housing prices is artificial. Meanwhile, former homeowners that have already left the property with the belief they lost the home to foreclosure are ending up on the hook for the unpaid debt, taxes and repairs.

When faced with reports on rising housing prices, reporters should ask some skeptical questions. Ask how sustainable those prices are if incomes are not rising. Ask how many houses are in the inventory available for sale and how many are off the market. Ask how many apartments are being warehoused (which some cities have laws against) and how this affects the prices renters are asked to pay.

In other words, go beyond the routine, superficial housing prices story, to try to get at what’s really happening out there.

Follow @USProjectCJR for more posts from this author and the rest of the United States Project team.

David Cay Johnston covers fiscal and budget matters for CJR’s United States Project. He is a reporter with 46 years of experience, including 13 at The New York Times; a columnist for Tax Analysts; teaches tax and regulatory law at Syracuse University Law School; and is president of Investigative Reporters & Editors (IRE). Follow him on Twitter @DavidCayJ.