Sign up for the daily CJR newsletter.

The top story in all the major papers on Wednesday was news that home prices jumped 11 percent in the first quarter from a year ago, further confirmation that the housing recovery is underway in earnest.

The double-digit home-price increases and return of bidding wars have led to an awful lot of “bubble” talk lately.

Gawker declared yesterday that “The Next Housing Bubble Is About To Pop All Over You.” Gawker doesn’t quite grasp that soaring prices in Silicon Valley and San Francisco are being driven by a flood of newly minted tech millionaires chasing after a constrained supply of higher-end homes, and that’s not a bubble. Bay Area transactions are still 16 percent below average levels over the last 25 years and half the level seen at the peak in the mid-2000s. Prices would have to skyrocket, as we’ll see below, to get back to peak levels.

Yahoo Finance also declared last week that “The Housing Market Gets Bubbly Again” in a confused piece largely based on one anecdote involving the author, who buries a second anecdote that contradicts his thesis.

Bloomberg headlined a story two weeks ago, “From Brooklyn to California, Housing Bubble Threat Grows.”

Bloomberg’s first anecdotal evidence of the bubble threat? “An open house for a five-bedroom brownstone in Brooklyn, New York, priced at $949,000 drew 300 visitors and brought in 50 offers.”

A five-bedroom brownstone in Brooklyn for under a million bucks—and it only drew 50 offers?

Its second anecdote is about an all-cash deal for a $2 million house in Menlo Park, aka Facebook headquarters.

Its third anecdote is no more impressive:

In south Florida, ground zero for the last building boom and bust, 3,300 new condominium units are under way, the most since 2007.

Does 3,300 sound like a lot of condos to you? In 2005, there were 50,000 condos in the pipeline in downtown Miami alone.

The BBC throws in with a terrible package on “Concerns over potential housing bubble in the US” in which the reporter explains bubble economics with this head-slapper:

The worry is: If prices are rising too high too fast, people will drop out of the market altogether, creating a bubble.

I know screaming “housing bubble” draws clicks and viewers, but no, we are not in another housing bubble.

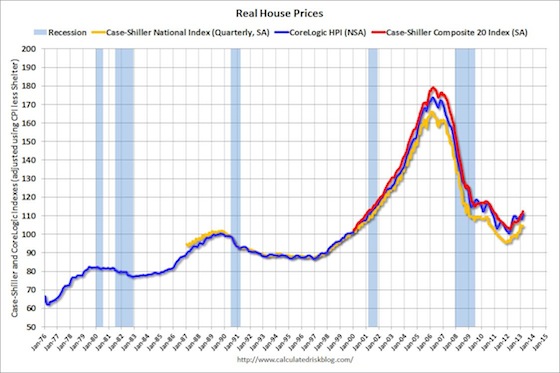

First, prices, as measured by Case-Shiller, are still down 27 percent from their peak seven years ago. But Case-Shiller calculates nominal prices, not real ones. And the consumer price index (inflation) is up 15 percent since 2006. So real house prices are about 37 percent below 2006 levels and are just now returning to where they were 13 years ago. Here’s a chart from the excellent Bill McBride of Calculated Risk showing real house prices going back a few decades:

Click here for a CR chart from last year that showed housing prices at about 1979 levels, by Robert Shiller’s measure, anyway.

And here’s a tip for the math-challenged out there: It takes a larger percentage increase to offset a percentage decline. Take a $100,000 house at the peak. If it fell the real national average 42 percent in the bust, it would have been worth $58,000 at the bottom early last year. But to get back to $100,000, it would take a 72 percent increase from the trough.

Even now, after the sharp bump off the bottom, prices would have to jump 60 percent to get back to their bubble-era peak.

It’s not just the national market, either. The bubble stories tend to focus on markets like Los Angeles and San Francisco. But both those markets, for instance, are just now getting back to 2003 and 2000 prices, respectively.

To get back to peak levels, San Francisco’s home prices would have to jump 60 percent, by my calculations (using Case-Shiller data). LA would have to jump 66 percent, Phoenix 99 percent, and Miami 105 percent. Las Vegas’s house prices would have to skyrocket 149 percent to reach record levels.

Not coincidentally, those markets are the ones where prices fell furthest. You also have to remember that some land-constrained individual markets are prone to booms and busts and probably always will be. Take LA. Its house prices crashed 40 percent in real terms from 1990 to 1997, soared 192 percent from 1997 to 2006, and then crashed 48 percent from 2006 to 2012. While individual regional bubbles aren’t fun, they’re not going to threaten the entire financial system like the more-or-less nationwide subprime bubble did between 2007 and 2009.

Now, you could argue that the bubble of the 2000s was so insane that we don’t have to get back to those levels to have another bubble. And that’s true, but there are plenty of other indicators that say we aren’t in one.

For instance, is it better to rent or to buy? It’s still better to buy, according to S&P Indices calculations:

The essential question regarding any bubble is: Does the investment make sense? Can homebuyers actually afford their mortgages?

Here’s a WSJ chart showing how historically cheap houses are (this goes through the third quarter of last year)

And S&P:

Homeowners are spending a historically low amount of their income on their mortgages—just 13 percent, according to Zillow. From 1985 to 1999, that number was 20 percent. In the bubble it was nearly twice what it is now. In 1979 it approached three times today’s levels.

You also have to ask about lending standards. Nobody cares if rich people are buying $2 million houses with cash. There are only so many of them, and if they lose their shirts, it affects them and, maybe, the help. The systemic problems come when banks lend to people who can’t afford to pay them back. Even Bloomberg’s bubble-threat story notes in its too-be-sure paragraph that “in contrast to the easy lending of the boom years, mortgage standards are strict.”

For instance, the average borrower closing a house in March had a 743 FICO score, according to Ellie Mae. The average denied applicant had a 702 score, just four points lower than the average approved applicant in 2007.

The Cassandras say the Fed is blowing bubbles with its easy-money policy. But the whole point of quantitative easing and extremely low interest rates is to fight the massive deflationary bias caused by trillions of dollars of bad debt incurred during the bubble. The economy can’t get back on its feet until housing starts really moving again. Low interest rates make it possible for buyers to afford higher prices. As interest rates start to rise in the next year or two, that will counterbalance the surge in prices, as will an increase in inventory, as underwater homeowners are able to sell their houses without losing money.

To really have a housing bubble, you have to have lots and lots of transactions. And while sales are up (remember, that’s a good thing!) they’re still at 1999 levels, even though we have 10 percent more households since then. Transactions of new and existing homes would have to pop 55 percent to reach peak bubble levels—roughly 3 million more deals a year.

That’s not happening anytime soon.

Bear markets don’t last forever, and not every recovery is a bubble.

Has America ever needed a media defender more than now? Help us by joining CJR today.