Sign up for the daily CJR newsletter.

With the government shutdown over, the political media is devoting more attention to problems with the Obamacare rollout–most glaringly, the errors and technical failures confronting consumers who try to shop for coverage on the new insurance exchange websites. In the last few days, however, GOP criticism and media coverage has come to focus on a different concern: the termination notices that many consumers enrolled in health insurance plans purchased on the individual market are receiving, often accompanied by offers to buy new insurance at a substantially higher price.

These notices contradict President Obama’s oft-stated promise that Americans who like their healthcare plan would be able to keep it as reform was implemented. Still, they should come as no surprise — this outcome was anticipated by health policy experts both within and outside the administration. Unfortunately, most media coverage before this week did not explain how the process was likely to play out or hold the president accountable for making promises he could never keep.

Obama repeatedly promised that Americans could keep their existing health insurance plan between 2008 and 2010, as this compilation video by New York magazine makes clear:

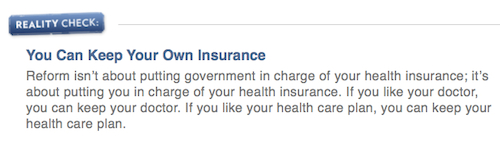

Moreover, those promises have not been retracted. Obama’s claims are still all over the White House website, including so-called “reality checks” like this:

Likewise, Obama’s statement on the third anniversary of the Affordable Care Act in March of this year reiterated the claim that, “If you like the plan you have, you can keep it.” On Monday, White House adviser Valerie Jarrett even took to Twitter to declare that “Nothing in #Obamacare forces people out of their health plans”:

FACT: Nothing in #Obamacare forces people out of their health plans. No change is required unless insurance companies change existing plans.

— Valerie Jarrett (@vj44) October 29, 2013

Jarrett’s claim followed a NBC story on how the “Obama administration knew millions could not keep their health insurance” that framed the issue as a cover-up. The reality is more mundane, however, as wonks like The New Republic‘s Jonathan Cohn have explained. The changes to the individual market that we are seeing were virtually inevitable due to the Affordable Care Act’s new requirements for minimum coverage and benefit levels. (Note: Most Americans receive group health coverage through their employers. That market will also change in some ways as a result of Obamacare but is not the focus of the current controversy.)

Many plans offered on the individual market did not meet these new standards. And while some existing plans were exempt from these requirements, the tight limits on changes that can be made to grandfathered plans under rules issued in 2010 have prompted many insurers to terminate them–an outcome that was foreseen even within the administration, as The Washington Post‘s Glenn Kessler notes. Of course, many of the people whose plans are being terminated may have access to plans that offer more robust coverage and/or new subsidies via the health insurance exchanges, once they are fully operational. But those benefits do not have any bearing on the truth status of Obama’s claims, which even supporters of health reform are now acknowledging.

A review of the earlier coverage of Obama’s promises shows that these likely complications were rarely raised by even respected political and health reporters. The pattern began during the 2008 campaign, when both Obama and Hillary Clinton tried to assure voters that they could keep their existing plan under healthcare reform. These claims received little attention. Here, for instance, is NPR’s Julie Rovner in August 2008 paraphrasing Obama’s promise without disputing it (at the time, Obama was touting a reform plan that did not include an individual mandate):

ROVNER: But what Obama is proposing isn’t really government-run health care. It doesn’t even have a requirement for individuals to have coverage, like the plans offered by his main primary opponents, John Edwards and Hillary Clinton. Obama says under his plan, if you already have insurance you like, you can keep it.

Sen. OBAMA: But if you’re one of the 45 million Americans who don’t have health insurance, you will have health insurance that’s available to you. No one will be turned away because of a pre-existing condition or illness.

Likewise, The New York Times quoted Obama’s promises without comment in reports from March and June 2009 as his salesmanship for the legislation ramped up:

Mr. Obama bypassed such difficult questions [about redistribution] on Thursday, and focused instead on areas of potential agreement.

“If we want to cover all Americans,” Mr. Obama said, “we cannot make the mistake of trying to fix what isn’t broken. So if you have insurance you like, you’ll be able to keep that insurance. If you have a doctor you like, you can keep that doctor. You’ll just pay less for the care that you receive.”

The pattern continued in a Washington Post report by Michael Shear on an Obama statement after the bill’s passage was assured in March 2010.

Of course, it was difficult to definitively check Obama’s promises before the final legislation was enacted. But it was always clear that the law would prompt changes in the health insurance marketplace, as a handful of important stories made clear. In June 2009, for instance, the Associated Press wrote that “His vow sounds reassuring and gets applause, but no president could guarantee such a pledge.” Similarly, The Washington Post‘s David S. Hilzenrath reported that Obama’s promise would “not necessarily be true.” These points were reiterated in a June 2010 report on the grandfathering rules-making process by Hilzenrath and N.C. Aizenman and an August 2010 explainer by Aizenman.

Interestingly, media factcheckers have only partly concurred with this pushback. Factcheck.org’s Lori Robertson, focusing on the employer-based market, reported in August 2009 that Obama “can’t make that promise to everyone”–a conclusion reiterated this week by both her colleague Brooks Jackson and Kessler, the Washington Post Fact Checker, who gave the president’s statements “four Pinocchios.” However, PolitiFact rated Obama’s claims “Half True” in 2009 and again in 2012–a confusing rating given a headline on the earlier piece which states, “Barack Obama promises you can keep your health insurance, but there’s no guarantee.”

So why did reporters so often fail to call Obama out on his claims? One problem is the media’s lack of interest in policy, particularly when assessing claims that are not definitively false (most coverage of the plan was published before it took effect). In this sense, Obama’s messaging strategy echoes the Bush administration, which frequently exploited this blind spot by promoting misleading or half-true claims that were difficult to factcheck and uninteresting or complicated to explain to readers. As I noted above, some major outlets did occasionally produce more critical policy coverage, but the cautions raised by those stories never became part of the larger media narrative.

Another possible explanation for the lack of scrutiny given to Obama’s promises is that the press often takes its cues about the flaws in a policy from the opposition party, which is part of a pattern of indexing coverage to the range of debate among political elites. In this case, conservative politicians and pundits often emphasized baseless charges like “death panels” or made speculative claims about how it is intended to undermine employer-provided insurance.

This coverage failure underscores the need for a vocal and reality-based opposition. Just as the divided Democratic opposition undermined the prominence of experts in weapons control during the debate over Iraq, Obama’s free pass on “you can keep it” illustrates how skeptical reporting depends on the combination of technical policy critiques and attention from opposition elites. If either component is absent, journalists are all too likely to miss the story.

Follow @USProjectCJR for more posts from this author and the rest of the United States Project team.

Has America ever needed a media defender more than now? Help us by joining CJR today.