Sign up for the daily CJR newsletter.

The New Republic‘s Jonathan Chait and Columbia’s Jeffrey Sachs rip into the Wall Street Journal editorial page for making some dumb errors in an editorial claiming that it’s numerically impossible to tax the rich enough to close the deficit.

Chait and Sachs note that the Journal disproves its own point, in part by making dumb or disingenuous arguments like this:

In 2005 the top 5% earned over $145,000. If you took all the income of people over $200,000, it would yield about $1.89 trillion, enough revenue to cover the 2012 bill for Medicare, Medicaid and Social Security—but not the same bill in 2016, as the costs of those entitlements are expected to grow rapidly. The rich, in short, aren’t nearly rich enough to finance Mr. Obama’s entitlement state ambitions—even before his health-care plan kicks in.

Chait eviscerates that paragraph:

Notice the sleight of hand here. They’re comparing the income of the over-$200,000 set for 2005 and comparing it not to the deficit — it is way larger than the deficit — but to the cost of running most of the government. But we don’t need the rich to fund all of Medicare, Medicaid and Social Security. Other folks earn money, too. Nobody is proposing to eliminate their taxes. Moreover, the Journal is comparing revenue from 2005 with outlays in 2012 and 2016. And, yeah, it’s always hard to pay for today’s government with a tax base from the smaller economy of ten years earlier.

The first thing to understand about the Journal edit page is that its primary motivation is to push policies—especially tax ones—that benefit the very rich. They hate antitrust enforcement, trade restrictions, social programs, progressive taxation, regulation, collective bargaining—anything that might restrain the folks at the very top of the heap from putting themselves further out of reach. Basically, if a robber baron in the late 19th century would have liked a policy, that’s what the Journal favors.

So the Journal performed this ludicrous thought experiment that claims that even if we taxed 100 percent of the top 1 percent’s income, it would only net the Treasury $938 billion. Sachs points out that the math is off by several hundred billion dollars. Since the top 1 percent had income of $1.7 trillion and paid $400 billion of it in taxes, the real number would be $1.3 trillion, more than enough to get the deficit down below historical levels this year and way more than enough to run huge surpluses for the next decade under either current law or the Obama budget.

But nobody, of course, is actually proposes taxing the rich at anywhere near 100 percent of their income, much less 50 percent. So let’s look at more realistic numbers.

First, here are some banana-republic stats Sachs points out:

The average income tax rate paid by the top 1% has declined from 34.5% in 1980 to just 23.27% in 2008. During this period, the share of total income accruing to the richest 1% has soared from 8.5% in 1980 to 20% in 2008.

It’s worth noting that the richest 0.1 percent pay even less than that 23.3 percent, mainly because, in perhaps the clearest signs of our government’s priorities, we tax investment income at less than half the rate we tax labor income.

So to continue the thought experiment, what if we taxed the top 1 percent at pre-Reagan, 1980 rates of 34.5 percent (the marginal rates were much higher at 70 percent, but I’m talking effective rates)? That would net us just roughly $190 billion over what the richest pay now, based on those 2008 numbers (which are sure to be low, as the rich have recovered nicely since then).

That alone would cut the CBO’s projected deficits, which after 2013 are back to more historically normal levels of around 3 percent, under current law by about a third over the next ten years and Obama’s by roughly a quarter.

But there’s another other big problem here. The Wall Street Journal has a long history of editorializing in favor of deficits and against balanced budgets. As it said a couple of years ago, “We’ve long argued that deficits per se are not worth losing sleep over.” It somehow forgets all about that here.

In other words, the deficit doesn’t have to go to zero, according to everything the Journal has ever said. Presumably the Journal doesn’t see the need for deficits to go below 2.9 percent of GDP, since that was the lowest number their hero Ronald Reagan posted in his eight years in office.

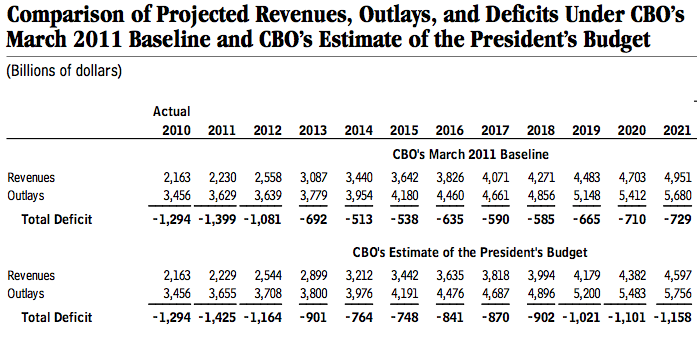

So here’s the Congressional Budget Office on what deficits look like as a percentage of GDP under both current law and the proposed Obama budget (click for a larger chart):

Under current law, the CBO projects deficits beginning next year of 6.9 percent, 4.2 percent, 3 percent, 3 percent, 3.3 percent, 2.9 percent, and 2.8 percent. It projects the Obama plan’s budget deficits at 7.4 percent for next year, and then 5.5 percent, 4.4 percent, 4.1 percent, 4.4 percent, 4.3 percent, and 4.3 percent thereafter.

Here are Reagan’s budget deficits from 1983 to 1988: 6 percent, 4.8 percent, 5.1 percent, 5 percent, 3.2 percent, and 2.9 percent.

Raising taxes on the top 1 percent back to pre-Reagan levels would drop the baseline and Obama budget deficits by roughly 1.2 to 1.3 percentage points of GDP per year (and presumably more, as income at the top has tended to rise far faster than the economy as a whole), putting both well below Reagan-era levels through 2020.

After that, Medicare costs have to be reined in or the deficits explode. Nobody I’ve seen questions that. The dispute is over how to do it.

Remember, these are just projections. The actual numbers will play out differently. But this is what we’ve got to work with now.

The bottom line: contrary to what the Journal says, raising taxes significantly on the top 1 percent would indeed make a significant dent in future deficits. Raising taxes less on the top 5 percent to 10 percent or even the top 25 percent, would narrow deficits even further. And that’s without even considering spending cuts.

We could work full time just picking apart the misleading stuff or outright falsehoods on the Journal edit page, but we’d go insane. As Chait says:

There’s always a problem involved in wasting one’s time examining very bad arguments. But organs like the Journal editorial page — which just won a Pulitzer Prize! — are influential and prestigious. I think very few people realize that these people are just pure clowns. They’re not messing up complex economic theories here. They’re messing up basic arithmetic.

Has America ever needed a media defender more than now? Help us by joining CJR today.